I. Introduction

More than three decades have passed since Korea adopted the local governance system. The first resident election of local council took place in 1991. How much has Korean local governance grown since then? According to J. Lee (2002), the catchphrase local government should be granted with decision-making, tax-collecting (tax-levying) rights and human resources was popular during decentralization movements decades ago. Decision-making rights meant delegation of authority, while tax-collecting rights signified financial decentralization and human resources emphasized local authority over arranging local government organization and human resource. For the past 20 years there have been efforts to delegate central government affairs and to promote autonomous organization and personnel in local governments. However, not much has been done with fiscal decentralization. Without fiscal decentralization, local governance would be incomplete. Delegation without autonomous financial resources will only burden local governments. Aside from the recent local consumption tax reform, it seems that the Moon Jae-in administration does not intend to make any further substantial attempts to achieve fiscal decentralization.

Then why is fiscal decentralization not happening? There are contesting views on fiscal decentralization. While most local governments ask for more fiscal independence and autonomy, some critiques accuse local governments of potential waste of financial resources with no significant improvement in public service performance (J. Kim, 2007, pp. 69–70; Weingeist, 2009, p. 285). Could it be perhaps there is no alternative to ideologies of balanced growth and financial equity? Fiscal decentralization consists of two components: decentralized taxation and decentralized expenditure. Decentralized taxation secures autonomy of a local government conditional with local accountability. On the other hand, decentralized expenditure guarantees autonomy and sufficiency of expenditure unconditional with how much cost a local government can afford on its own.

In the past, the Korean government promoted an economic growth model based on low-cost manual labor. Low-cost production was possible partly due to population concentration in the Seoul metropolitan area and the consequent abundant supply of labor. Thus, migration to Seoul from all over the nation was not deemed a serious problem back in the 1960s-1970s. Since then, economic disparity between metropolitan areas and suburban areas have severely worsened, widening the gap in population, capital, and housing prices. These gaps resulted in imbalanced taxation among local governments.

Consequently, decision makers chose to increase financial resources dedicated to local government expenditures rather than delegating national tax revenue to local government tax revenue. The main purpose was to mitigate local government financial imbalances, based on a national consensus on local equality (J. Lee, 2002). What could we expect if a significant local delegation of national tax revenue takes place? As of now, although new tax items and delegation take place, most taxes are collected from the Seoul metropolitan area, resulting in an exacerbated financial disparity between the Seoul metropolitan area and suburban areas. In contrast, there are greater demands of per capita local government expenditures in rural areas mainly due to greater proportion of low-income seniors in the population. Under this tax environment it is challenging to adhere to the law of settlement and accountability in taxation (tax revenue)-expenditure. This is the reason Korean decentralization policy have emphasized decentralized expenditure more than decentralized taxation (Jung, 2011).

If fiscal decentralization were to emphasize more of fiscal autonomy of a local government than delegation of tax revenues and fiscal authority, would there be an alternative policy? In terms of tax revenue, demand for balanced growth and fiscal equity may deter further fiscal decentralization. On the other hand, fiscal decentralization that focuses on fiscal expenditure could bring forth a variety of solutions. However, one could hardly expect improvement in public service performance and efficient resource allocation without the local government being accountable for its own revenues and expenditure. It is natural to consider a fiscal policy efficient when local governments are responsible for collecting their own local tax and non-tax revenues. Then, we must investigate whether this natural doubt has been empirically tested: Are local public services better in local governments with the law of self-financing (accountability)? Are they better when local governments are endowed with sufficiency and decision-making authority over the use of financial resources? If the level of tax decentralization is the same in different local governments, do decentralized expenditure account for better public service? In contrast, under the same degree of decentralized expenditure, would local governments with higher decentralized taxation provide better public service?

This research analyzes fiscal decentralization in terms of autonomous taxation (decentralized taxation) and autonomous fiscal expenditure (decentralized expenditure). It aims at an empirical investigation on whether fiscal decentralization affects public service performance. Most previous studies have not associated fiscal decentralization and local government performance directly, especially not in terms of individual public services. Aside from its focus on fiscal decentralization and local government service performance, this study may also be distinguished by its comparative investigation of local governments within a single country’s policy context. It is more convenient to detect the true effects of fiscal decentralization in within-country analysis than in cross-country analysis. Main analysis is based on a combination of quantitative data on local government finance and qualitative data on public service performance.

II. Theoretical Background

1. Local Government Finance in the Korean Context

1) Administrative district system

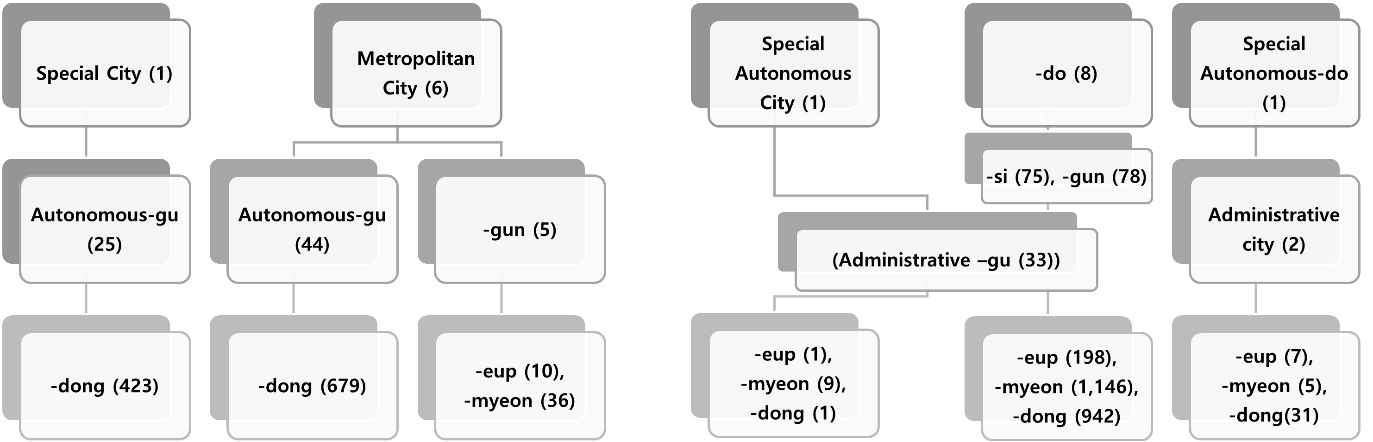

Korean local governments are categorized into special city, special autonomous city, metropolitan cities, do (province), special self-governing province, si (city), gun (county) and gu (district; municipal government). Seoul, which is the capital of Korea, is a special city. Metropolitan cities consist of Busan, Daegu, Incheon, Gwangju, Daejeon and Ulsan. There is one special autonomous city: Sejong. There are 8 do’s: Gyeonggi-do, Gangwon-do, Chungcheongbuk-do, Chungcheongnam-do, Jeollabuk-do, Jeollanam-do, Gyeongsangbuk-do and Gyeongsangnam-do. There also is one special self-governing province, Jeju. Si, gun and gu’s are part of province. There are gu’s in special cities and metropolitan cities, and in some cases there are guns in some metropolitan cities[1]. While there are other administrative districts that belong to lower hierarchies of the system, such as eup, myeon and dong, they are usually not considered as level of analysis in most local government studies in Korea. This is because administrative heads of these lower-level systems are not elected but appointed. However, eup, myeon and dong are considered preliminary means of public service delivery, and a few studies have recently emphasized their importance. Figure 1 below shows different types of administrative local governments in Korea. Numbers in parentheses represent numbers of respective types of local governments.

2) Local government revenue system

Before beginning discussions on measurement of fiscal decentralization, it is important to briefly investigate the structure of Korean local government revenue system. Revenue structure of local government is presented in Table 1. Items in this table will be referenced numerous times in the later sections of this paper. Some are more important than others because they are part of significant indices that will be used as major variables in the research model.

2. Fiscal Decentralization Performance and Measurement

1) Conceptualization (Definition) of fiscal decentralization

Fiscal decentralization may be defined by various conceptualizations. Scholars often analyze different cases, which often leads to a variety of definitions as scholars moderate the concept for their analysis. Most studies that involve comparative analysis on fiscal decentralization often define fiscal decentralization by referring to the proportion of local government tax revenue in the national tax revenue. They emphasize the relationship between central government and local governments. This perspective defines fiscal decentralization as a delegation of taxation and expenditure authorities and operations from the higher government to lower government (Ha & Moon, 2013).

On the other hand, some define fiscal decentralization as a degree of fiscal autonomy. This definition may apply to comparative studies on local governments. Cha (2011) describes fiscal decentralization as “local government’s authority to acquire financial resources independently and use them autonomously, without interference or control by the central government.” Strictly speaking this is rather a definition of fiscal autonomy, which is a result of fiscal decentralization. However, in most comparative studies on local governments, the term fiscal decentralization is preferred over fiscal autonomy. This study will also follow the prevalent term to minimize confusion.

While decentralized taxation focuses on increasing fiscal accountability of a local government based on its self-determined taxation, decentralized expenditure emphasizes increasing autonomy on financial resources that may be expended at local government’s autonomy. In other words, decentralized taxation means a delegation of national tax sources to local tax revenue; and decentralized fiscal expenditure means an expansion of local subsidies and grants. However, increasing national government subsidies comes at the cost of autonomous expenditure plan of a local government. It would not be considered as an effective means of enhancing fiscal decentralization.

2) Effects of fiscal decentralization

Researchers from various academic backgrounds have conducted studies on the effect of fiscal decentralization. Tiebout (1956), famous for his introduction of the phrase “voting by feet”, discovered an improvement of quality and quantity of local government public service under fiscal decentralization. Oates (1972) suggested that fiscal decentralization promotes efficient allocation of resources, thereby causing an increase of social welfare and economic growth. Oates (1993) later classifies efficiency of fiscal decentralization into allocative efficiency and productive efficiency. Allocative efficiency is an idea that a local government that is physically close to residents is more likely to meet their preferences than a government that is not as close (Hayek, 1945; Musgrave, 1969; Sow & Razafimahefa, 2015, p. 3; Tiebout, 1956). Productive efficiency points out that local governments that understand distinct characteristics of their regions and reflect heterogeneity across jurisdictions can produce and supply better public goods at a lower cost (Kwon, 2011, p. 162). Oates’s studies have influenced numerous succeeding researchers, leading to major emphasis on the effect of fiscal efficiency on economic growth.

Most prevalent in this area are studies on the economic efficiency of local finance and an increase of accountability as a product of fiscal decentralization (Bahl & Linn, 1992, pp. 59–75; Cha, 2011; Dabla-Norris & Wade, 2002, pp. 4–12; De Mello, 2000, pp. 3–30; Ebel & Yilmaz, 2002; Shah et al., 1994, p. 44). Other studies have analyzed the effect of fiscal decentralization on fiscal integrity (soundness) (Jung, 2011) and the effect of fiscal decentralization on mitigation of corruption and promotion of transparency (Bird & Vaillancourt, 1998; A. Kim, 2018; Moon & Bok, 2009; Treisman, 2000, pp. 399–457; Weingeist, 2009, pp. 1–31).

In addition, different researchers have also explored the effect on economic growth (B. Choi & Jeong, 2001; J. Choi, 2015; Ha & Moon, 2013; Hong, 2013; Im & Cho, 2008; Koo, 2015), the effect on national competitiveness (Ha & Moon, 2013), and the effect of decentralization on the employment of young adults (J. Lee & Lim, 2018).

3) Measuring fiscal decentralization

Previous studies have either measured fiscal decentralization as 1) the proportion of local government tax revenue and expenditure in the national tax revenue and government expenditure, or 2) the proportion of local tax and non-tax revenues and autonomous fiscal resources in the local government gross tax revenue and gross expenditure, respectively. Most comparative studies on different countries have focused on the national-local difference in government tax revenues and expenditures, by measuring the proportion of local government tax revenue and expenditure in the gross national government tax revenue and expenditure. In contrast, studies on difference between local governments on the level of fiscal decentralization (in most cases, studies on fiscal autonomy) have measured fiscal decentralization as the proportion of local tax and non-tax revenues in the gross local government tax revenue (decentralized taxation) and the proportion of autonomous fiscal resources in the gross local government expenditure (decentralized expenditure).

Specifically, Koo (2015) compares different countries on their levels of fiscal decentralization and economic growths. In Koo’s study, fiscal decentralization is measured in two aspects: decentralized taxation and decentralized expenditure. Decentralized taxation is conceptualized as the proportion of gross local government revenue in the gross national government revenue, while decentralized expenditure is the proportion of gross local government expenditure in the gross national government expenditure, respectively. Variables used in these conceptualizations all originate from the International Monetary Fund (IMF)'s Government Finance Statistics (GFS). Ha & Moon (2013)'s study on fiscal decentralization and national competitiveness also measures decentralized taxation as the proportion of local tax and non-tax revenues in the gross national tax revenue and the proportion of local tax and non-tax revenues in the gross amount of local government revenue. Decentralized expenditure is measured as the proportion of local government expenditure in the gross government expenditure. Including Koo’s and Ha et al.'s studies, quite a few studies have adopted indices from IMF’s GFS and OECD indicators (Akai & Sakata, 2002; Davoodi & Zou, 1998).

On the other hand, Cha (2011)'s research on Korean local governments defines decentralized taxation as proportions of a local government’s local tax and subsidy revenue in the gross annual settlement of tax revenue. J. Choi (2015) in his comparative study on Korean local governments introduces two distinct indices on decentralized taxation and decentralized expenditure. Fiscal decentralization index in terms of taxation is measured as the proportion of local tax revenue out of the sum of national government transfer and local tax revenue. In terms of expenditure, it is measured as the proportion of the local government expenditure out of the gross amount of government expenditure in the local area. Moon & Bok (2009) conceptualizes fiscal decentralization as the proportion of autonomous financial resources out of total fiscal expenditure of a local government. In addition, Jung (2011) considers per capita local tax revenue and per capita grant and subsidy revenue as a key indicator of fiscal decentralization. Cha (2011)'s fiscal decentralization index consists of the proportion of self-obtained local tax revenue in the gross annual settlement of local tax revenue, proportion of local grant in the gross local tax revenue, proportion of local grant in the gross local tax revenue, proportion of costs of local government’s own projects in the gross local government expenditure. J. Lee & Lim (2018) analyzes the effect of decentralized taxation on young adult employment, by considering Financial Independence Ratio and Financial Autonomy Ratio as key variables.

As we have seen in previous studies on fiscal decentralization, varying measurement and conceptualization are mostly due to differing levels of analysis: cross-country or local government comparison. Strictly, fiscal decentralization is the level of delegation of fiscal authority from central government to local governments. It is therefore more appropriate to conduct a country-level analysis. However, some downsides of country-level analysis include, but are not limited to, the dearth of country-level samples and a variety of political, economic, and cultural environment of countries. Universal analysis of different countries’ fiscal decentralization may not always be a viable option. As an alternative, most studies focus on the varying independence and autonomy of local governments, an aspect of local government fiscal decentralization. Decentralized taxation and decentralized expenditure may result in different effects over different local governments. For instance, Yong-in-Si with a relatively high Financial Independence Ratio is considered highly fiscally decentralized. In contrast, Yangyang-Gun, a county government but with a relatively low Financial Independence Ratio, is considered not as highly fiscally decentralized. Such conceptualization does not strictly abide by the popular definition of fiscal decentralization, but it does provide some insights on the fact that it is more convenient to control exogenous factors in comparative studies on local governments than on different countries.

This study will investigate effects of fiscal decentralization on local governments’ public service performances. Cross-country comparisons are less likely to be equipped with contextual differences on each country’s public service delivery, thus making it inconvenient to detect the true effects of fiscal decentralization. This study will instead compare local governments in Korea, of which their policy contexts are more likely to be identical to each other’s. It will analyze local tax revenue (excluding local government grants) and non-tax revenue (Financial Independence Ratio) as a proportion of general accounting tax revenue in terms of decentralized taxation. In terms of decentralized expenditure, it will analyze proportions of local tax revenue and autonomous fiscal resources in general accounting tax revenue.

3. Local Government Performance

It is challenging to accurately define performance of a local government because varying perspectives exist. Park & Kim (2000) defines local government performance as “the ultimate effect of core local government public services on residents’ welfare.” Ko (2013) categorizes (local) government performance as internal management effectiveness, outputs and outcomes, and accountability on citizens (residents). Most studies in the past have emphasized a local government’s capacity on internal management. Government performance may be represented by either objective evaluation on suppliers’ side or subjective evaluation on customers’ side (Song, 2003). While objective evaluation in the suppliers’ perspective is usually based on official public data that is likely to assure objectivity of the evaluation, performances that are easily quantifiable add to major drawbacks including failure to account for equity, responsiveness, or quality of service (H. Lee & Kim, 2014). Citizen perspectives on and evaluation of local government performance have become increasingly important. If citizens are at the center of our attention, their subjective and qualitative evaluations on public service are considered performance of a local government (Ho & Coates, 2004). Advantages of subjective evaluation by citizens include differentiation between citizens’ priorities and bureaucrats’ priorities in terms of providing and benefiting from public services, and an ability to measure responsiveness to citizens’ demands, consequently (Han, 2009). On the other hand, there are also disadvantages of subjective evaluation. Measurement errors are commonly brought up by those who are against subjective evaluation (T. Kim, 2003). These errors may occur because objective outputs of public service are not significantly correlated with subjective performances (Brown & Coulter, 1983; Higgins, 2005; Stipak, 1979). Citizens also do not have complete and accurate information about public service when they are asked to evaluate performance (Boyne, 2003; Kelly & Swindell, 2002). Their self-identified roles as customers or partners of government may also affect expectation towards and satisfaction in public services (H. Choi & Lee, 2020). Despite potential concerns regarding the subjectivity, citizens’ evaluation may provide essential information in the decision-making processes of different levels of government (Poister & Henry, 1994). G. Lee (2004) suggests citizen evaluation to include both customers who have directly experienced particular public service but also others that have no such experience. Pollitt (1988) also points out that citizen perception is essential to evaluating quality and effectiveness of public service because the ultimate goal of such service is to improve welfare of citizens. Recent examples of this perspective include, but are not limited to, H. Lee & Kim (2014) and H. Lee & Lee (2014). These studies have considered individual performances on public transportation, recreational parks, and sanitation as a local government’s performance.

It is easier to measure a local government performance than to measure a central government performance because of several aspects of the former: local governments’ homogenous tasks come with a large comparison pool, repetitive and standardized daily work, are based on benefit principle, are highly accessible by customers (citizens), and there are relatively small window between the time of service delivery and citizen evaluation (Pollitt et al., 1994). On the other hand, there are measurement difficulties due to local governments’ intangible public goods and monopolized service provision as well as unclear causal relations. Therefore, local government performance is measured by either internal management capacity of a government or citizen satisfaction rate. Internal management capacity is essentially a government capacity to use financial and human resources (input) to produce public service output, assuming high internal management capacity brings high public service quality. In contrast, citizen satisfaction on local government public service emphasizes service outcome over output. Satisfaction rates on individual services compared to expectation are often used because overall satisfaction rates are prone to subjective perspectives on government and expected service quality in general. H. Lee & Kim (2014) and H. Lee & Lee (2014) both measure citizen satisfaction rate compared to expected service level and satisfaction rate on individual public services, each of which is based on subjective perceptions of citizens on local government performances.

In this study, local government performance is measured by subjective perceptions of citizens, both performances on individual services and overall performance. The main analysis is on the effect of fiscal decentralization on individual public service performance and overall satisfaction rates.

4. Fiscal Decentralization and Local Government Performance

Most previous studies have not associated fiscal decentralization and local government performance directly. Most of them have investigated promotion of efficiency, economic growth, promotion of transparency and accountability due to fiscal decentralization, but not much on an individual public service perspective.

How does fiscal decentralization affect local government public service performance? First of all, in terms of decentralized taxation, high level of fiscal decentralization is likely to cause a government’s attention on citizens’ demands, who pay taxes to a government. This will in the end promote efficient allocation of resources and enhanced performance. A local government may encounter tax boycotts by citizens as in the case of California’s Proposition 13, so it will try its best to deliver efficient public service to them. However, proportion of local tax revenue in the gross national tax revenue is not as big as it is in the U.S., thus alleviating local governments’ accountability with self-financed revenues.

Second, in terms of decentralized expenditure, unlike local governments with government subsidy that has a pre-specified purpose of expenditure, those with more independent local tax and non-tax revenues are likely to be responsive to citizens’ needs. These local governments will try to provide public services preferred by their citizens, which will lead them to focus on improving service performance, quality and quantity. In other words, public services that are universally provided by the central government may not be able to fully consider local-specific characteristics and local residents’ needs. In contrast, those with more autonomous fiscal resources, local tax and non-tax revenues are more likely to satisfy the needs and preferences of residents and local-specific characteristics with their expenditure and public service performance.

Then which would have a greater effect on local government performance—decentralized taxation or decentralized expenditure? In countries like Korea where the level of independence over taxation is relatively low, decentralized taxation would be expected to have a smaller effect on government performance than decentralized expenditure. Firstly, local governments in Korea operate by expending national tax that is granted to each local government according to its financial status, with the addition of local tax that is collected based on the decentralized local taxation system universally applied in Korea. Despite the same tax items and tax rates, local governments have varying taxation capacities and environments (e.g. business-friendly decision making, urban planning and natural endowment/resources, preference of residents) along with different expenses. Therefore, it is meaningful to compare the impact of decentralized taxation on performance of different local government entities.

Following research hypotheses are derived from discussions above.

-

Hypothesis 1. Decentralized taxation is positively related with local government performance.

-

Hypothesis 2. Decentralized fiscal expenditure is positively related with local government performance.

-

Hypothesis 3. Decentralized fiscal expenditure has a greater positive effect on local government performance than decentralized taxation does.

III. Research Methods

1. Research Model

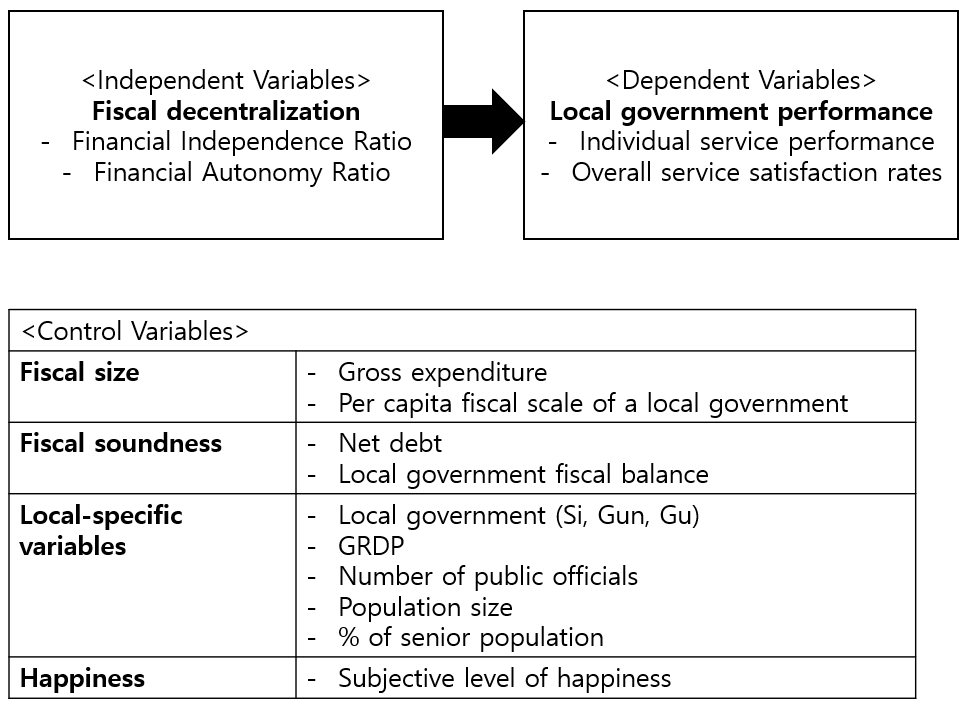

Figure 2 demonstrates the research model of this study. The purpose of this research model is to investigate the effect of fiscal decentralization on local government performance. Fiscal decentralization is measured by Financial Independence Ratio and Financial Autonomy Ratio, while local government performance consists of individual public service performance and overall citizen public service satisfaction rates. A variety of factors may affect local government performance. Among them is no fixed set of fiscal decentralization control variables that are known to affect government performance; there have not been a lot of previous studies regarding the matter. This study controls for fiscal size, fiscal soundness and local-specific variables, each of which could affect local government performance. Individual perceptions are controlled by subjective happiness of citizens. To sum up, this study controls for local government fiscal size represented by following variables: gross local government expenditure and per capita fiscal scale of a local government. It controls for fiscal soundness represented by net size of debt, local government fiscal balance[2], local government (Si, Gun and Gu), number of public officials, population, proportion of senior population and gross regional domestic product (GRDP). Lastly, subjective level of happiness is controlled for.

2. Data and Methodology

The dataset used in this study originate from three different sources. First, data for local government performance are sourced from Korean Local Government Public Administration Service Satisfaction Survey conducted in 2015 and 2016 by the Center for Survey Research (CSR) in the Graduate School of Public Administration, Seoul National University. In October 2015, survey was targeted at resident satisfaction rates on public administrative services provided by Si and Gun local governments. In October 2016, survey was targeted at autonomous Gu (district) local governments and Si and Gun local governments in Gyeonggi-do (province). For both years the survey agent Matrix Corporation dialed to samples of respondents that had been distributed based on residing areas, gender and age of population (primarily categorized by residing areas and then extracted proportional to gender and age). The valid sample sums up to 41,910 for both years; 19,760 in 2015 and 22,150 in 2016.

Second, data for subjective levels of happiness are sourced from the Integrated Survey on the Role of Government and Quality of Life conducted in 2013 by the Center for Survey Research (CSR). Gallup Korea was an agent of the survey project; it surveyed adult residents of 230 Si, Gun and autonomous Gu for 23 days from January 29th, 2013 and 30 days from October 31st, 2013. 21,050 respondents are among the samples that have been quota-sampled by residing areas, gender and age. At least 100 respondents have been sampled for each local government.

Lastly, fiscal decentralization variables and other control variables have been sourced from Local Finance Integrated Open System and Information on My Local Government. Level of analysis is city, county and municipal governments, which are Si, Gun and Gu.

3. Variables

1)Independent Variables

Fiscal decentralization is the independent variable of this study. As discussed earlier in the measurement of fiscal decentralization, operational definition of fiscal decentralization is often the proportions of local tax and non-tax revenues and autonomous financial resources in the gross tax revenue and gross fiscal expenditure, respectively. This study analyzes two aspects of fiscal decentralization and their effect on local government performance: decentralized taxation and decentralized expenditure. For these two aspects, Financial Independence Ratio and Financial Autonomy Ratio are used, respectively. Both of these variables are from Local Finance Open System’s annual settlement data.

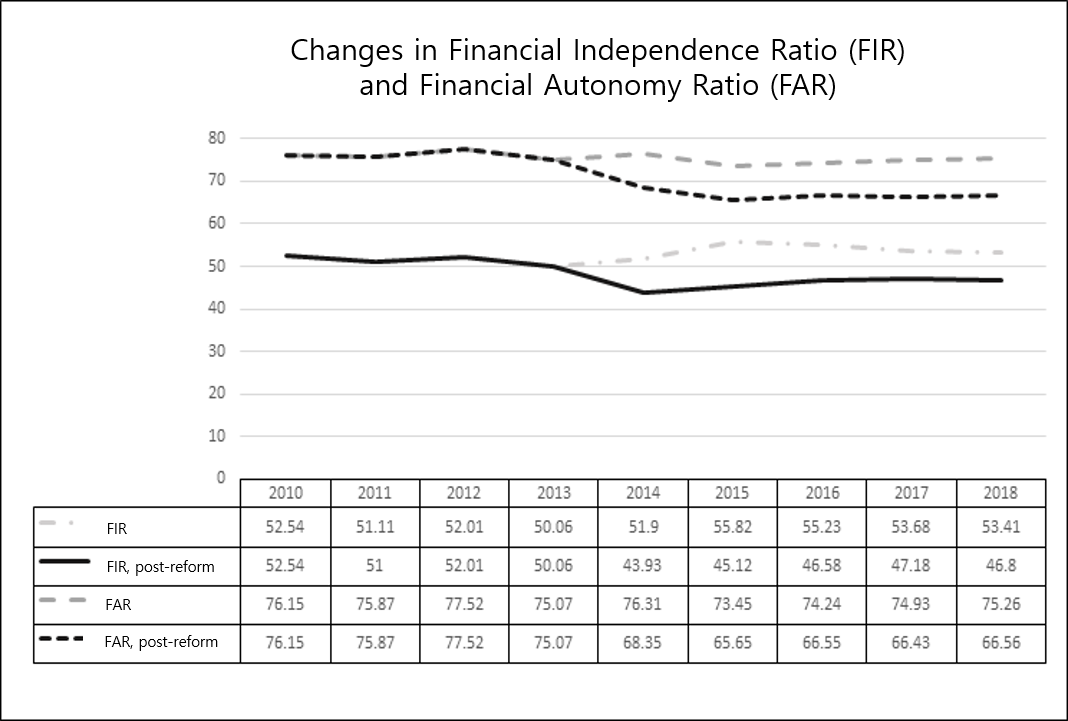

Financial Independence Ratio is the proportion of local tax revenue (excluding local education tax) and non-tax revenue in the general accounting tax revenues. Financial Autonomy Ratio is the proportion of local government financial resources that local government is authorized to plan and execute budget on, which consist of local tax and non-tax revenues and autonomous financial resources in general accounting tax revenue. The main reason previous studies do not include Financial Independence Ratio and Financial Autonomy Ratio is that balance carried over and transfers are included in non-tax revenue of a local government, causing a major disparity with the actual non-tax revenue. From 2014 tax revenue accounts have been revised to exclude leftovers, carryovers, transfers and deposits. Therefore Financial Independence Ratio has become a more accurate representation of a local government’s self-reliant fiscal operations, and Financial Autonomy Ratio better portrays the proportion of self-reliant planned and executable financial source of revenues. This study adopts post-2014 revision of tax accounting in Korean local governments.

Figure 3 illustrates changes of Financial Independence Ratio and Financial Autonomy Ratio over 2010-2018. Both Financial Independence Ratio and Financial Autonomy Ratio have fallen after the non-tax revenue revision in 2014 and no significant change is observed. However, 65.1% of local governments (158 out of 243) has Financial Independence Ratio less than 30%. This shows that decentralized taxation in local government has not advanced well. In contrast, Financial Autonomy Ratio that represents decentralized expenditure ranges from 65% to 66%, meaning that local governments depend on local government grants. Local government grants are granted by the central government with no pre-specified purposes; as they are part of general accounting resources, local governments have autonomy to spend them at their will. One of the drawbacks of local government grants is that they are synchronized with national tax, which makes them sensitive to business cycles. Thus, local government grants do not guarantee a stable financial operation of a local government.

2) Dependent Variables

Satisfaction rates on 14 individual public services have been obtained on a 10-point Likert scale. Respondents were asked to answer to “How much are you satisfied with the following public service provided by the local government (Si or Gun) of your residence?” If they were very satisfied, they were to give 10 points; if they were very unsatisfied, they were to give 0 point. In addition, overall satisfaction rates have been obtained through a question “Including all individual services you have marked satisfaction rates on, how much are you satisfied with the overall public service provided by the local government of your residence?” Table 2 presents the 14 individual public services in the survey.

As mentioned previously, satisfaction rates on local government services are operationalized as a variable of local government performance. We assume that satisfaction rates on individual services are more likely to be a proximate measurement of citizens’ perceptions on government performance than overall satisfaction rates on local governments are. Averages of overall satisfaction rates and individual service satisfaction rates have both been included in the research model; averages of overall satisfaction rates are operationalized as citizens’ satisfaction, while averages of individual service satisfaction rates are local government performances.

Table 3 shows the top 15 local district governments for government public service performance, which is the dependent variable of this study. Gwacheon-si has the highest average satisfaction rates of 14 public services, and these results are generally consistent with objective measures of local government performance.

3) Control Variables

Control variables of this study include local government gross expenditure and per capita fiscal scale of a local government, both of which represent the size of local government finance. Both variables are sourced from Local Finance Open System as of year 2015. Also included as control variables are net debt and local government fiscal balance, which represent fiscal soundness of a local government. Local government (si, gun, gu), number of public officials, population, proportion of senior citizens, gross regional domestic product and subjective level of happiness also comprise of control variables. Subjective level of happiness was collected in 2013, and all other control variables are as of 2015.

IV. Results

1. Descriptive Statistics

Presented below in Tables 4 and 5 is descriptive statistics of variables included in the research model. Local government performance averages at 6.4 out of 10, ranging from 5.9 to 7.0. Financial Independence Ratio averages at 20%, with a minimum of 4.29% and maximum of 56.41%. Financial Autonomy Ratio averages at 52%, with a minimum of 27% and maximum of 74%.

Table 5 illustrates local government performance (citizens’ satisfaction rates) on individual service areas. The lowest performance on average was observed in economy, which averaged at 5.57 out of 10. Rural development and childcare were the areas next lowest in service performance. The highest performance was observed in sanitation, which averaged at 7.31, and public transportation at 7.0.

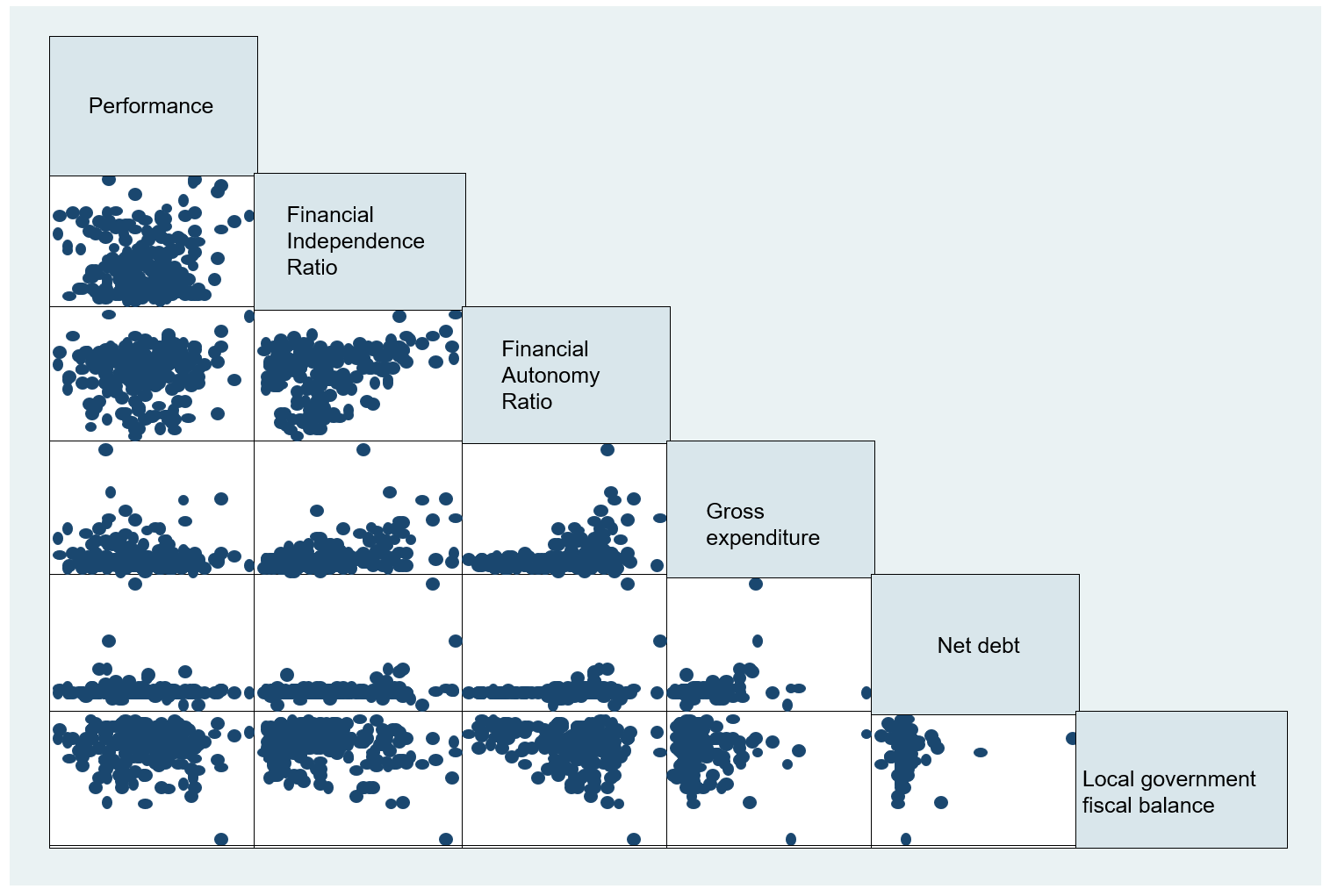

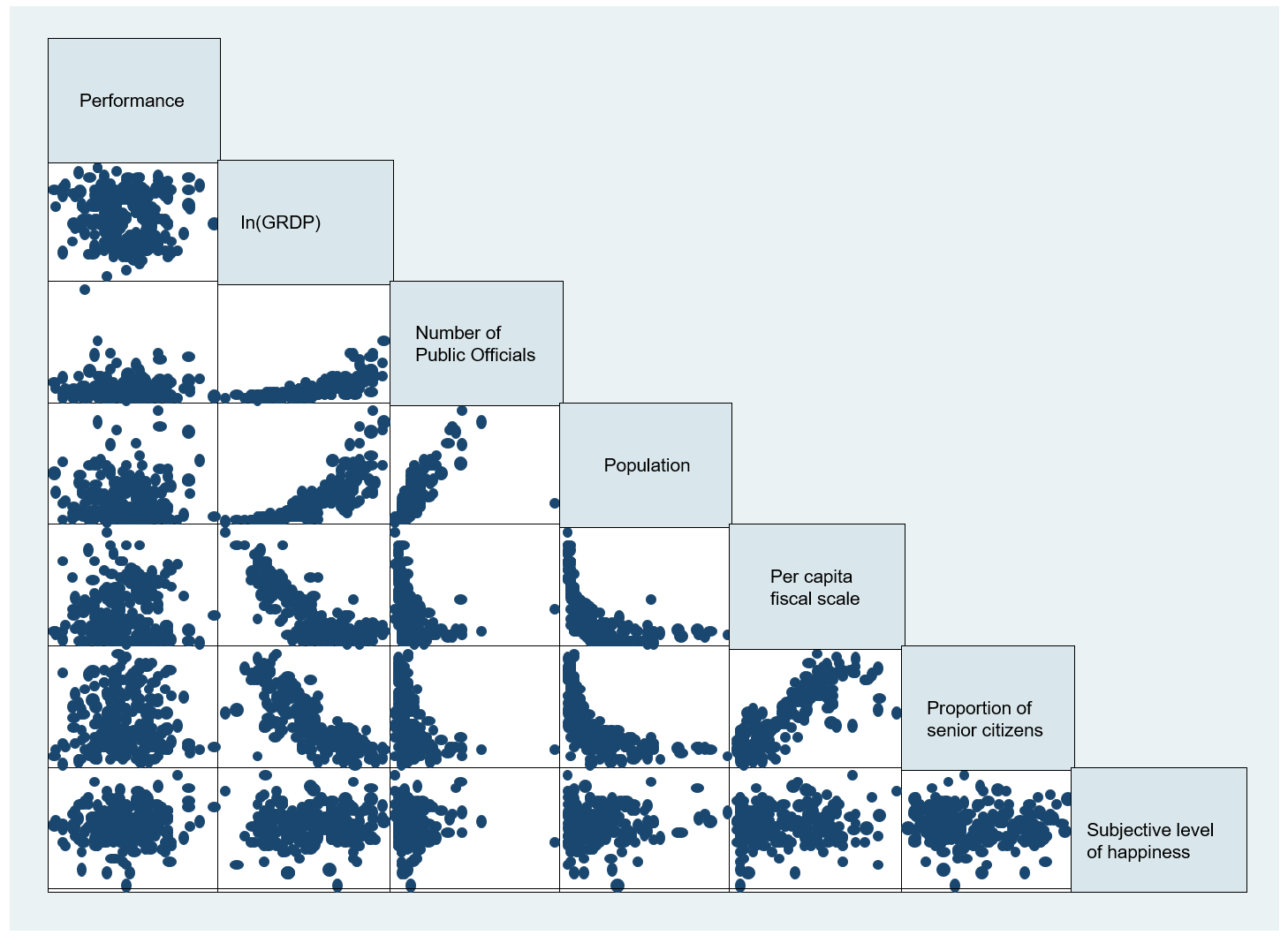

Figures 4 and 5 below depict correlations among variables included in the research model. High correlations can be observed between number of public officials and population. Financial Autonomy Ratio and Financial Independence Ratio have a correlation of 0.272, and the highest correlation of 0.866 was observed between number of public officials and gross expenditure. It is conventional to remove either number of public officials or population from the model if they were key variables of interest, we have decided to keep them as control variables in the model.

2. Regression Analysis: Overall performance

Table 6 contains regression results on the two models that contain individual service performances and overall satisfaction rates as dependent variables, respectively. The research model with individual service performance (satisfaction rates) also includes Financial Independence Ratio and Financial Autonomy Ratio as independent variables.

In the model with overall satisfaction rates as a dependent variable, the causal relationship between the fiscal decentralization variable and the dependent variable was not statistically significant. The overall satisfaction rates was negatively related with net debt and positively related with per capita fiscal scales of local governments, proportion of senior citizens and subjective level of happiness. In contrast, the average of individual service satisfaction rates (performance), a dependent variable in the other model, was found to be in statistically significant relationships with fiscal decentralization variables. In models 1 and 2, the dependent variable and Financial Independence Ratio and Financial Autonomy Ratio (fiscal decentralization variables) were in positive relationships. However, in the model 3 where both Financial Independence Ratio and Financial Autonomy Ratio were included as variables(?), the causal relationship between the dependent variable and Financial Independence Ratio was no longer statistically significant. Financial Autonomy Ratio was still in a statistically significant relationship with the average individual service satisfaction rate.

The gross expenditure was in a negative relationship with the fiscal decentralization performance, while local government fiscal balance was in a negative relationship when the local government fiscal balance had a lower proportion of deficits.

Next, in models 2 and 3, gu regions have shown better performance than gun regions (reference dummy variable). Larger gross regional domestic product was related with lower performance rate, and this is because GRDP causes an increase in Financial Independence Ratio and fiscal demand in the region at the same time. Under the same Financial Independence Ratio, an increase in GRDP lowered the performance of a local government. The number of public officials was in a positive relationship with local government performance; because population was controlled in the research model, an increase in the number of public officials cause an improvement in local government performances (measured by satisfaction rates on public services) at the same population size. In contrast, only in the model 2 was the population in a statistically significant yet low positive relationship with local government performance. The subjective level of happiness was in a positive relationship with performance, and this seems to be in concordance with subjective characteristics of perception surveys.

3. Regression Analysis: Individual public service performances

In this part, the effect of fiscal decentralization on local government performances of 14 individual public services. Regression results on Tables 7 and 8 show that Financial Independence Ratio is in a statistically significant relationship with performance of a local government’s public order services. Financial Autonomy Ratio was in a statistically significant positive relationship with disaster prevention, health and medical services, rural development, public transportation, culture, tourism, public order and park services. We can assume that these results are due to greater decentralized taxation and a local government’s greater investment in these services.

V. Conclusion

Does fiscal decentralization improve local government performance? Korea’s greater emphasis on decentralized expenditure than on decentralized taxation deterred fiscal accountability of local governments. There have been concerns on potential waste of financial resources and local government administration capacities, with no substantial improvement in performance. Unlike most prior studies, this study associates fiscal decentralization and local government performance directly, particularly in terms of individual public services. Aside from its focus on fiscal decentralization and local government service performance, this study can also be distinguished by its comparative investigation of local governments within a single country’s policy context. It is more convenient to detect the true effects of fiscal decentralization in within-country analysis than in cross-country analysis. In addition, this study also separates fiscal decentralization into decentralized taxation and decentralized expenditure for more detailed analysis of fiscal decentralization and its impact on local government performance. Based on survey on citizen satisfaction rates from si, gun, and gu level local governments, the results of this study, at least in some respect, answer the question.

Our analysis shows that both Financial Independence Ratio, which represents decentralized taxation and Financial Autonomy Ratio, which represents decentralized expenditure, have positive effects on a local government performance. Interestingly, in the research model that included both variables, the effect of decentralized taxation on the government performance was not statistically significant. Meanwhile, the positive effect of decentralized expenditure was statistically significant. Results show that decentralized expenditure does not necessarily hinder local government performance, unlike many concerns.

Development gaps between Seoul metropolitan area and non-capital areas, and gaps between smaller si, gun and gu level local governments have intensified due to earlier imbalanced growth strategy by the Korean government. Tax sources have thus been unevenly distributed, causing potential imbalances among regions as decentralized taxation becomes more common. Therefore, despite widespread demand for decentralization, measures for fiscal decentralization have not been adopted immediately. There have been numerous concerns on decentralized expenditure; people claim probable inefficiency in a local government’s fiscal operations that lack accountability. According to the analysis from this study, that is not necessarily true. Korean local governments do not have authority to decide on tax items for their local tax revenues; every local government shares the universal local tax items. There may be slight differences in flexible tax rates or regional resource and infrastructure taxes. In general, citizens do not differentiate local tax from national tax. Local tax commonly has different tax items and tax rates over different local governments in most other countries, but this is not the case in Korea. Citizens are not able to compare which local government levies less tax or more tax. Under this homogenous local tax structure, decentralized taxation does not guarantee the accountability of local governments.

It is advised that Korea emphasize decentralized expenditure more than decentralized taxation. Decentralized expenditure does not hinder local government performance, and thus Korean government should continue to promote it to resolve imbalances across local governments.

Local government grant has been fixed at 19.24% of the national tax since more than 14 years ago. It is important to increase the proportion of local government grant in the national tax. In addition, regarding allocation of local government grants, there are criticisms that polices do not regard recent population changes across local governments (H. Lee & Seong, 2019). Local government grants should be distributed according to population size of a local government, and it is also important to identify any redundancies granted to gun regions with decreasing population. Lastly, it is advised that the proportion of local government grants in the national tax should be fixed for si, gun and gu regions, respectively.

This study has examined the relationship between fiscal decentralization and local government performance with Korean local government data. Preliminary level local governments were primarily considered in the analysis because they have a greater variety (more than 200 compared to 17) than local governments of higher levels (metropolitan cities and provinces). Moreover, it is appropriate to refrain from comparing different levels of governments (preliminary level - si/gun/gu - and metropolitan cities/provinces altogether). In addition, whether the analysis is also applicable in other countries may be determined only after extensive cross-country comparative studies of local government fiscal decentralization and local government performance. Universal and general implications regarding our findings are contingent on the availability of universal measures of local government performance (both quantitative and qualitative). As of now, it is not convenient to measure and directly compare performances of different local governments around the world. The primary reason is that different countries have different decentralization system and consequently, public service provided by local governments vary across the world. In addition, expectations from citizens may also vary, making satisfaction rates difficult to compare in different countries. This manuscript has thus focused on Korean local governments, that are based on the universal national taxation and decentralization system yet with diverse spending structures. However, we expect that our implications may provide insights for further research that deals with local governments in different countries, by comparing them both nationally and internationally. We expect further research on administrative and fiscal decentralization system in different countries will enable us to conduct analysis that accounts for different systems and consequently, obtain generalizable results.

Acknowledgements

This research was supported by Daejeon University Research Grants (2020).